Insurance Certificate Management for Small Business Owners

Master insurance certificate tracking with proven systems that protect your business from costly lapses. Learn how to manage COIs efficiently, avoid compliance gaps, and streamline vendor verification.

Aaron Kushner is an entrepreneur with decades of hands-on experience running service companies and eCommerce operations. He founded DocuStrong to solve the compliance and document-tracking challenges he faced firsthand in the field.

Your largest client just called-they need confirmation that your subcontractor’s insurance is current within the hour. After searching through folders and emails, you discover the certificate expired three weeks ago. Project delayed, relationship strained.

This scenario is common. Insurance certificate management rarely gets attention until something goes wrong. For small business owners juggling multiple vendors and compliance requirements, tracking Certificates of Insurance (COIs)-documents proving a business has valid insurance coverage-quickly becomes overwhelming.

In this comprehensive guide, you’ll discover practical systems for managing insurance certificates, learn how to avoid costly compliance gaps, and implement strategies that protect your business. Whether managing your first contractor or dozens of vendor relationships, these proven approaches help you stay organized, compliant, and focused on growth.

Who Needs COI Management?

Certificate tracking is essential for any business working with third parties. Construction companies need COIs from subcontractors. Property managers require them from maintenance vendors and cleaning crews. Healthcare facilities verify insurance for staffing agencies and equipment suppliers. Service businesses need COIs when hiring specialists. Retailers must provide COIs to landlords when leasing space. If your business hires contractors, works with vendors, or enters service agreements, effective COI management protects you from liability gaps and compliance violations.

What Is a Certificate of Insurance and Why Does It Matter?

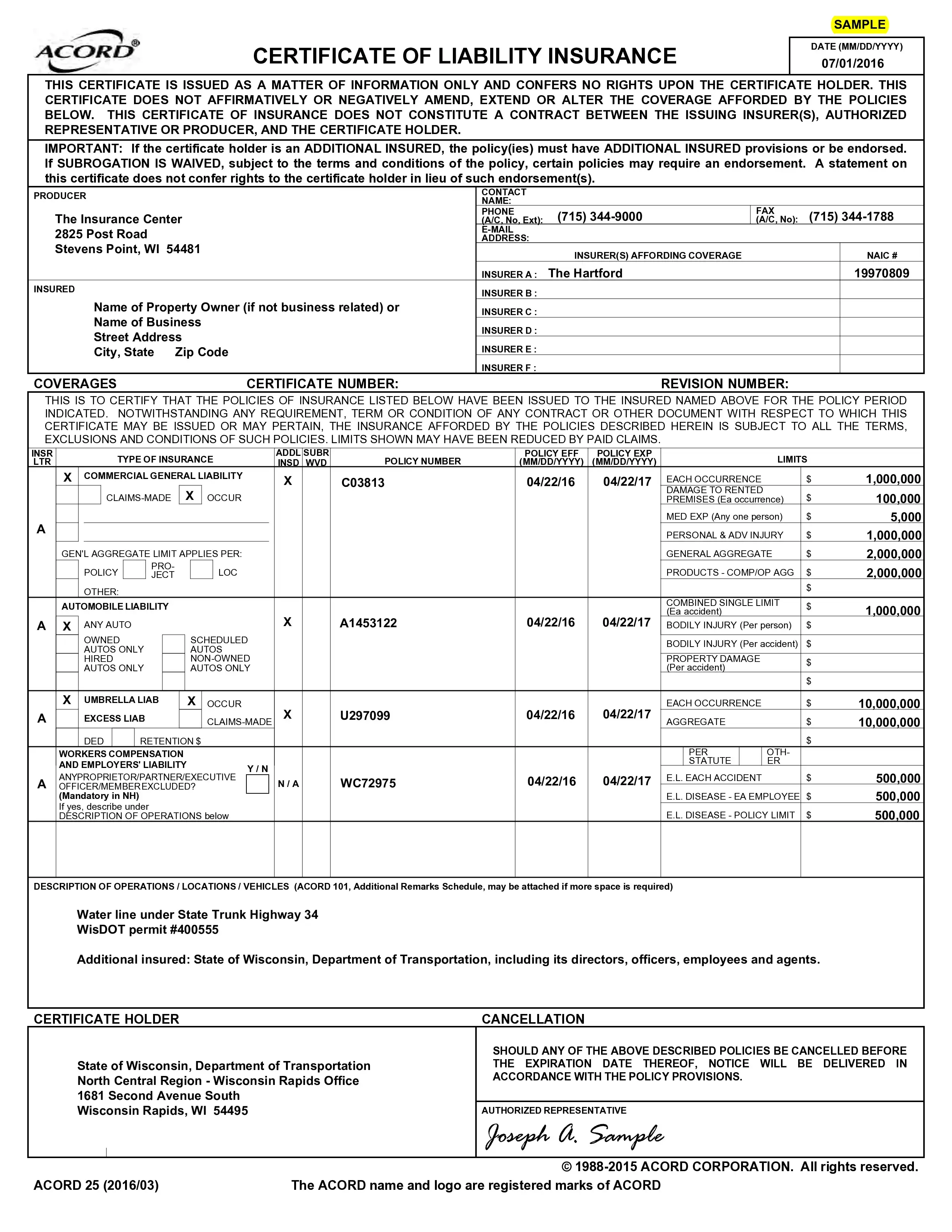

A Certificate of Insurance (COI) is a standard document that serves as proof of a vendor’s insurance coverage, summarizing policy limits, effective dates, and types of coverage. More specifically, it’s a one-page document that verifies a business or individual holds valid insurance protection, providing essential policy details including coverage types, limits, effective dates, and the insurance carrier’s contact information without requiring you to review the entire insurance policy.

Insurance certificate management is the process of collecting, verifying, and tracking proof of insurance for vendors, contractors, and partners. COI tracking means monitoring vendor insurance documents for validity, accuracy, and expiration dates.

According to industry research from Insureon, COIs serve as proof of an effective risk management plan, giving clients and partners financial protection against losses and damages. Most COIs follow the standardized ACORD 25 form developed by the Association for Cooperative Operations Research and Development, which became the industry standard in the 1970s to eliminate confusion and create consistency across insurance companies. ACORD forms are widely used but not legally mandated.

For small business owners, COIs function as a critical risk transfer mechanism. When you hire a contractor, vendor, or subcontractor, their COI confirms they have adequate coverage to handle incidents that occur during their work. Without proper verification, your business could be held financially responsible for accidents, property damage, or injuries caused by third parties you’ve hired.

Is a COI the Same as Proof of Coverage?

A COI does not provide coverage; it only summarizes policy details. The certificate is issued as a matter of information and serves as evidence that an insurance policy exists, but it’s not the actual insurance contract. The policy itself is the binding legal document between the insured and the insurance carrier. While a COI provides convenient proof that coverage exists at a specific point in time, it doesn’t guarantee coverage will apply to every situation or that the policy won’t be canceled. For high-risk contracts or critical vendor relationships, you may want to request copies of the actual policy declarations page in addition to the standard COI.

The Real Cost of Poor Certificate Management

Manual COI tracking isn’t just inconvenient-it’s expensive. Businesses that rely on spreadsheets, email folders, or paper files to manage certificates face several hidden costs:

Financial exposure

- Working with an uninsured or underinsured vendor can trigger claims against your own insurance policy

- Even if claims are ultimately denied, according to Small Business Administration risk management guidance, gaps in vendor insurance verification can significantly increase your insurance costs and liability exposure

- You may be denied coverage entirely in cases of negligence in verifying vendor insurance

- Direct liability for accidents or damages when vendors lack adequate coverage

Operational delays

- Discovering an expired COI when a vendor is scheduled to start work creates immediate project delays

- Deadlines slip and budgets expand with every postponement

- Your reputation for reliability takes a hit with clients and partners

- Last-minute scrambling to find replacement vendors or alternative coverage

Compliance penalties

- In construction, general contractors may face fines for allowing uninsured subcontractors on job sites, depending on state and local regulations

- Healthcare facilities and property managers risk regulatory violations during inspections if vendor insurance lapses aren’t addressed

- Contract breaches when you can’t demonstrate vendor compliance

- Potential litigation from clients or property owners

Administrative burden

- Industry reports show that automated COI tracking significantly reduces manual follow-up and administrative workload

- Hours spent chasing vendors for renewals, verifying certificates, and tracking expiration dates

- Team members diverted from revenue-generating activities to manage paperwork

- Increased error rates from manual data entry and tracking methods

Understanding Certificate of Insurance Components

Before you can effectively manage COIs, you need to understand what information they contain. Every ACORD 25 certificate includes these critical sections:

Policyholder and producer information: The insured party’s business name (which should match your vendor exactly) and details about the insurance agent or broker who issued the certificate.

Insurance carrier details: The company providing coverage and their contact information. Verify the carrier’s financial stability through AM Best ratings-look for A- or higher ratings to ensure the insurer can pay claims.

Coverage types and limits: Specifics about each insurance type (general liability, workers’ compensation, commercial auto, professional liability) including policy limits per occurrence and in aggregate.

Policy dates: Effective and expiration dates that confirm insurance is currently active. An expired certificate means the vendor is potentially uninsured and non-compliant.

Certificate holder: Your business name appears here, indicating you requested the COI. However, being a Certificate Holder does not guarantee you will be notified of cancellation. Standard ACORD forms explicitly state that notification is governed by the policy, not the certificate. You must request a Notice of Cancellation Endorsement to be legally guaranteed an alert if the vendor’s policy is canceled or materially changed.

Additional insured status: This section indicates whether your business is named as an additional insured on the vendor’s policy. This designation is crucial-it means their insurance extends some coverage to your business if a covered incident occurs during their work. Most carriers require an endorsement (such as CG 20 10 or CG 20 37) for additional insured status to be valid, so always request a copy of the actual endorsement form to verify coverage is included in the policy, not just listed in the description box.

For example, a retail business hiring a contractor to renovate their storefront benefits significantly from additional insured status. If the contractor’s employee damages an adjacent business’s window, without additional insured status the retail business could be named in the lawsuit. With it, the contractor’s insurance typically defends both parties.

What Businesses Should Require in a Certificate of Insurance

While specific needs vary by industry and risk tolerance, these baseline requirements provide a starting point:

General Liability: $1 million per occurrence, $2 million aggregate minimum for third-party bodily injury and property damage.

Workers’ Compensation: Required for contractors with employees. Some states require sole proprietors or LLC owners to carry coverage depending on work performed.

Commercial Auto Liability: Required when vendor work involves driving, typically matching general liability limits.

Professional Liability: For consultants and specialized service providers protecting against negligence or mistakes.

These are general guidelines, not legal advice. Develop specific requirements with your insurance broker and legal counsel based on actual risk exposures.

Common Situations Requiring Certificate of Insurance Verification

Hiring Contractors and Subcontractors

Any time you bring in external workers for specialized tasks-from HVAC repairs to website development-verify their insurance coverage. Understanding COI requirements for contractors protects you from liability gaps. How to verify a COI starts with comparing the certificate against your documented requirements, then confirming policy details directly with the carrier for high-value projects.

What to look for: General liability ($1M per occurrence, $2M aggregate minimum), workers’ compensation for employees, and professional liability for specialized work.

Leasing Commercial Property

Landlords require tenants to provide COIs before signing leases. Your lease specifies required coverage types and minimum limits, typically including general liability and workers’ compensation. The landlord should be listed as certificate holder and additional insured.

Vendor and Supplier Relationships

Maintain current COIs for regular vendors-cleaning services, delivery companies, maintenance providers. Coverage should match the vendor’s activities: commercial auto for deliveries, general liability for on-premise services.

Event Planning

Event vendors should carry general liability insurance covering specific event dates. Verify venues have property insurance and adequate liability coverage.

Why COI Tracking Matters for Compliance, Contracts, and Risk Management

Systematic COI tracking isn’t optional-it’s fundamental business protection:

Contract compliance: Most business agreements require proof of insurance before work begins. Without current COIs, you’re in breach of contracts and may face penalties or project termination.

Risk mitigation: Small businesses should verify COIs directly with insurers for high-risk projects, ensuring protection from liability transfer failures where assumed vendor coverage has gaps or exclusions.

Operational continuity: Automated COI management prevents lapses through expiration tracking and renewal notices, eliminating project delays and emergency scrambling from discovering expired coverage.

Ready to Simplify Your Certificate Management?

Stop chasing paperwork and start protecting your business. Set up automated COI tracking in under two minutes.

Start Your Free Trial →

Building an Effective COI Management System

Small businesses can implement effective systems with the right framework. Here are the essential steps:

Step 1: Centralize Your Documentation

The foundation of good COI management is having all certificates in one accessible location. DocuStrong’s automated insurance compliance software provides centralized storage that eliminates frantic searching when you need to verify coverage quickly.

Create a consistent filing structure: Organize certificates by vendor name, project, or department. Include the policy expiration date in filenames for quick reference (e.g., “ABC_Contractors_GL_2025-12-31.pdf”).

Digitize everything: Paper certificates get lost or damaged. Scan all physical COIs and maintain digital versions for easier sharing and backup.

Maintain historical records: Insurance coverage liability extends beyond the policy period-archived certificates can be crucial during future disputes about incidents that occurred while coverage was active. This is critical for complying with state Statutes of Repose, which allow claims to be filed years after work is completed.

Step 2: Establish Clear Collection Processes

Having a standard process for requesting and receiving COIs ensures nothing falls through the cracks.

Build it into onboarding: Make COI submission mandatory before any vendor begins work. Include specific requirements in contracts.

Use standardized requests: Clearly specify coverage types, minimum limits, additional insured status, and special endorsements. Provide your business information exactly as it should appear on the certificate.

Set internal deadlines: Require COIs at least two weeks before a vendor’s start date, allowing time to address deficiencies without project delays.

Step 3: Implement Systematic Review

Receiving a COI is only half the battle-verify it meets your requirements using this 7-Point COI Review Checklist:

- Business name matches vendor exactly

- All required coverage types present

- Policy limits meet minimum requirements

- Effective dates cover the project timeline

- Your business listed as certificate holder

- Additional insured status included where required

- No concerning exclusions noted

For high-risk projects, verify directly with the carrier using the phone number on the certificate-not one provided separately by the vendor. Document your review and any accepted exceptions.

Step 4: Track Expiration Dates Proactively

The most common COI failure is letting certificates expire. An expired COI provides no coverage verification.

Set multiple reminders: Create alerts at 90, 60, 30, and 7 days before expiration. This graduated approach gives vendors time to renew and you time to follow up.

Monitor ongoing relationships: DocuStrong’s automated expiration tracking provides automated reminders ensuring you never miss renewal deadlines.

Have a contingency plan: Document your procedure if a vendor’s insurance lapses-suspending access, using alternative vendors, or obtaining short-term coverage.

Never Miss a COI Renewal Again

Automated expiration tracking with multi-channel reminders keeps your business protected.

Get Started Free →

Common COI Mistakes to Avoid

Even well-intentioned businesses make critical errors in certificate management. Watch out for these frequent pitfalls:

Accepting expired COIs: An expired certificate provides zero protection. Always verify that coverage is current before allowing vendors to begin or continue work. Set reminders well before expiration dates to request renewals with time to address issues.

Not verifying coverage limits: Don’t assume the limits listed on a COI are adequate. Compare them against your documented requirements and the actual risk exposure. A $300,000 policy might seem substantial until a serious incident exceeds it.

Missing additional insured endorsements: The COI description box is only a summary and does not confirm coverage is included in the policy. Always request the actual endorsement form (like CG 20 10 or CG 20 37) to verify your additional insured status is part of the policy, not just mentioned in the notes.

Relying on paper storage: Physical certificates get lost, damaged, or misfiled. Without digital backups, you have no proof of coverage verification if questions arise during audits or claims. Scan and digitally archive all COIs immediately upon receipt.

Failing to verify authenticity: Certificate fraud does occur in the industry. For significant contracts, always verify COIs directly with the insurance carrier using contact information you look up independently, not numbers provided by the vendor.

Certificate of Insurance Management Best Practices

These practices help small businesses maintain exceptional COI management:

Standardize Your Insurance Requirements

Create clear, written insurance standards for different vendor types. Having tiered requirements-“Standard,” “Enhanced,” and “High-Risk”-helps you apply appropriate standards consistently. Make these available to vendors before they bid on projects to ensure transparency and reduce negotiations.

Build Strong Vendor Relationships

Frame insurance requirements as partnership in risk management, not bureaucratic hurdles. Educate vendors about why you need specific coverage and respond promptly to their COI submissions-aim for 2-3 business day turnaround on reviews.

Leverage Team Collaboration

Use team collaboration features to distribute COI management responsibility. Designate primary and backup reviewers for different vendor categories, and create clear escalation protocols for questionable certificates.

Technology Solutions for Certificate Management

Spreadsheets work for a handful of vendors but quickly reveal limitations as you grow. Modern insurance certificate tracking systems offer features designed for compliance management.

DocuStrong’s compliance and security features provide centralized storage, automated expiration alerts, and verification workflows eliminating manual oversight. Automated COI management systems request updated certificates based on expiration dates, reducing administrative workload. Advanced platforms identify compliance gaps and flag them immediately.

Dedicated COI expiration tracking monitors all vendor certificates simultaneously with dashboard views of upcoming renewals and compliance status. Analytics capabilities show which vendors provide timely renewals and where bottlenecks occur. Integration with existing systems creates seamless workflows between accounting software and compliance tracking.

Transform Your COI Management Today

Join businesses using DocuStrong to automate certificate tracking and eliminate compliance gaps.

Start Free Trial →

Essential COI Management Checklist

Collection: Written requirements by vendor category • Standard request template • Two-week pre-work submission deadline • Additional insured requirements communicated

Review: Standardized verification checklist • Designated reviewers • Carrier verification for high-value contracts • Documentation of exceptions

Monitoring: Centralized storage • Multi-stage reminders (90/60/30/7 days) • Regular compliance audits • 10-year archive retention • Vendor suspension procedures

Team Coordination: Primary and backup reviewers assigned • Escalation process defined • Regular training • Communication protocols established

Frequently Asked Questions

How long should I keep expired certificates of insurance?

Keep expired COIs for at least 10 years, or indefinitely if stored digitally. Insurance liability extends beyond active policy periods-incidents that occurred while coverage was active can result in claims filed years later. Statutes of limitation and Statutes of Repose vary by state and can extend a decade past project completion, particularly in construction. Digital storage makes long-term retention simple and ensures you have coverage evidence for historical periods without physical storage costs.

What should I do if a vendor’s insurance expires mid-project?

Immediately stop all work until you receive proof of renewed coverage. Contact the vendor to request an updated certificate and verify renewal with their carrier. Document the work stoppage and delays. Never allow work to continue without valid insurance-the risk exposure far exceeds temporary delays.

Can I accept lower insurance limits than I typically require?

Reducing requirements should be a deliberate, documented decision based on scope of work, engagement duration, vendor track record, and potential exposure. Document your risk assessment and reasoning for any exception. For ongoing relationships or larger projects, maintain standard requirements consistently.

How do I verify a certificate is legitimate?

Always verify by contacting the insurance carrier directly using the phone number on the certificate-not contact information provided separately by the vendor. Confirm the policy is active, coverage types and limits match the certificate, and your business is properly listed. Watch for signs of fraud: poor print quality, missing ACORD standardization, unusual formatting, or vendor reluctance to allow direct verification.

What’s the difference between certificate holder and additional insured?

Certificate holder status simply means you receive the COI. Being listed as the certificate holder does not guarantee cancellation notification unless the policy includes a specific Notice of Cancellation Endorsement. Additional insured status extends the vendor’s insurance coverage to your business for claims arising from their work-meaning their insurance will defend and potentially pay claims on your behalf for covered incidents, significantly reducing your risk exposure.

Taking Control of Your Insurance Certificate Management

The businesses that excel at COI management have better systems, not bigger teams. They’ve recognized that certificate tracking is a strategic function that protects their operations, relationships, and bottom line.

Start with the foundational steps: centralize documentation, establish clear collection processes, and create systematic review procedures. These basics eliminate most compliance gaps and protect you from costly surprises.

As your vendor relationships grow, technology can scale your efforts without scaling your workload. DocuStrong’s comprehensive features transform certificate management from a time-consuming manual process into an automated system that runs reliably in the background.

The cost of proper COI management is measured in hours and systems. The cost of poor certificate management is measured in lawsuits, penalties, delays, and damaged relationships.

Ready to Simplify Your Certificate Management?

Stop chasing paperwork and start protecting your business. DocuStrong provides everything small businesses need to manage insurance certificates, licenses, permits, and compliance documents in one centralized platform.

Start your free trial today and set up your first automated renewal reminder in under two minutes. No credit card required.

Start Your Free Trial | Explore All Features

For more resources on small business compliance and document management, read our comprehensive Business Compliance Document Management Guide, visit our Small Business Resources category, or return to the DocuStrong homepage to learn more about how DocuStrong transforms compliance management for businesses of all sizes.

Related Articles

New Business Owner? Here Are the 12 Documents You Need From Day One

Starting a business without the right documents is like building a house without a foundation. Learn which 12 critical documents every new business owner needs to stay compliant, protected, and ready for growth from day one.

Annual Business License Renewals: A Month-by-Month Planning Guide

Master your business license renewals with this strategic month-by-month planning guide. Learn how to avoid penalties, streamline compliance, and never miss a critical deadline again.

Required Documents and Compliance Checklist for Hiring Your First Employee

A comprehensive guide to the essential documents, certifications, and federal and state compliance requirements for new employers, including EIN, Form I-9, W-4, and workers' compensation insurance.